Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What’s Ahead for Home Prices in 2023

What’s ahead for home prices in 2023 is a popular question. Over the past year, home prices have been a widely debated topic. Some have said we’ll see a massive drop in prices and that this could be a repeat of 2008 – which hasn’t happened. Others have forecasted a real estate market that could see slight appreciation or depreciation (depending on your area of the country). And as we get closer to the spring real estate market, experts are continuing to forecast what they believe will happen. Let’s read on to see their forecast.

Here is what the experts have to say:

Selma Hepp, Chief Economist at CoreLogic, says:

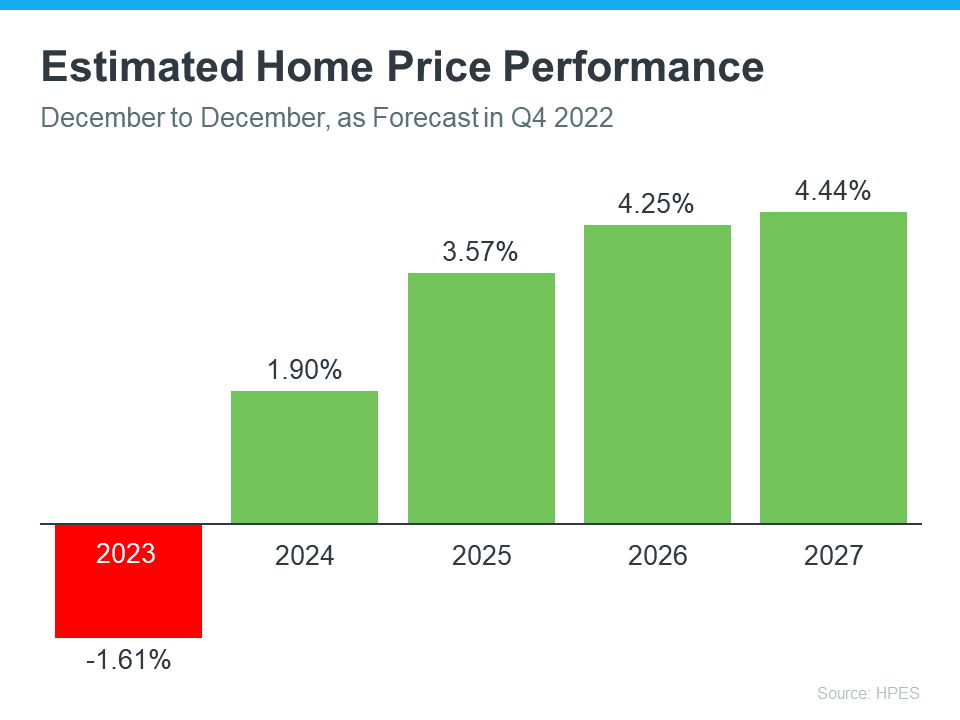

“While 2023 kicked off on a more optimistic note for the U.S. housing market, recent mortgage rate volatility highlights how much uncertainty remains. Nevertheless, the continued shortage of for-sale homes is likely to keep price declines modest, which are projected to top out at 3% peak to trough.”

Every quarter, Pulsenomics surveys a panel of over 100 economists, investment strategists, and housing market analysts regarding their five-year expectations for future home prices in the United States. Here’s what they said most recently:

Why should I consider buying now?

So, given this information the question you might be asking is: should I buy a home this spring? Here are three reasons you should consider making a move:

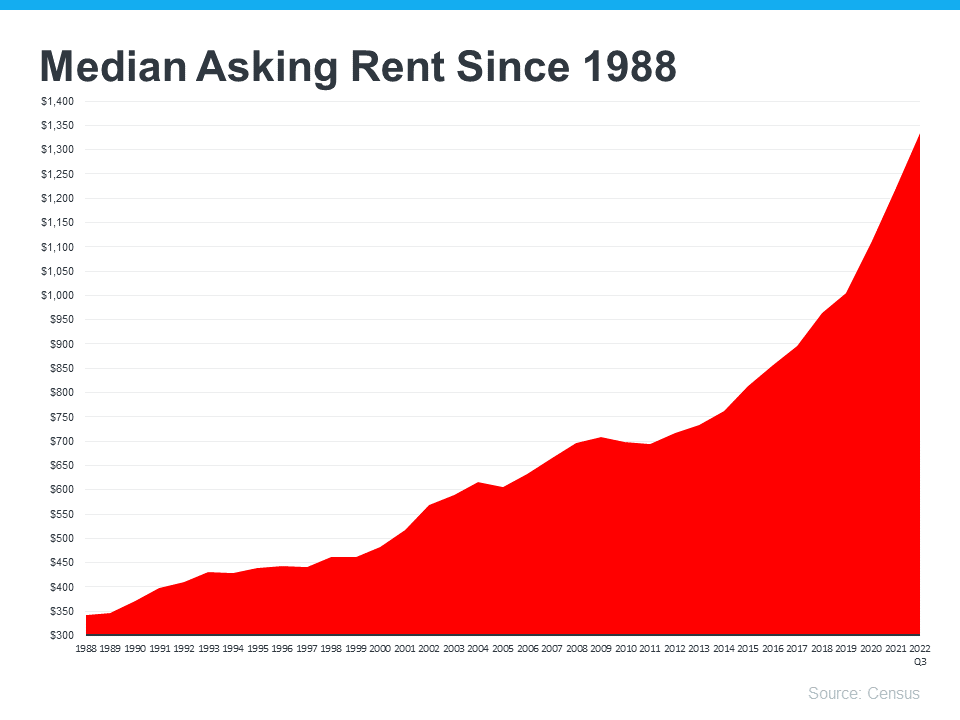

- Buying a home helps you escape the cycle of rising rents. Over the past several decades, the median price of rent has risen consistently. The bottom line is, rent is going up.

- Homeownership is a hedge against inflation. A key advantage of homeownership is that it’s one of the best hedges against inflation. When you buy a home with a fixed-rate mortgage, you secure your housing payment. So it won’t go up like it would if you rent.

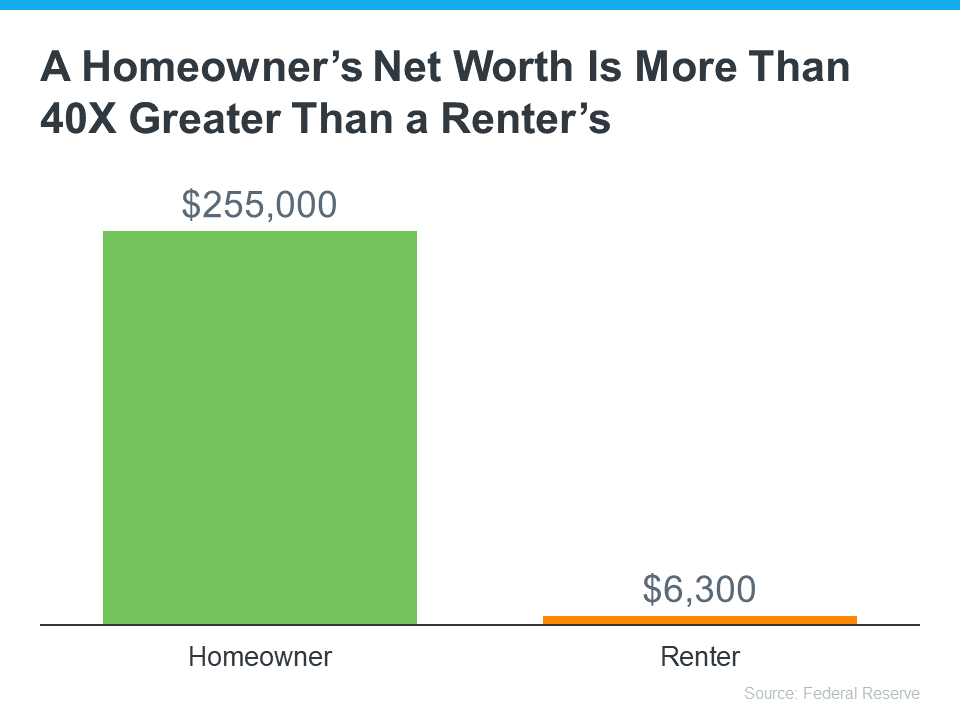

- Homeownership is a powerful wealth-building tool. The average net worth of a homeowner is $255,000 compared to $6,300 for a renter.

Experts are projecting a slight price depreciation in the housing market this year. This will be followed by steady appreciation. Given that, you may be wondering if you should move ahead with buying a home this spring. The decision to purchase a home is best made when you do it knowing all the facts. Having an expert on your side will increase your odds for success. Reach out and lets visit about your specific situation.

![Homeownership Builds Your Wealth over Time [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/01/26130518/Homeownership-Builds-Your-Wealth-In-The-Over-Time-MEM-1046x2314.png)